Cash Flow vs Profit: What New Zealand Business Owners Often Get Wrong

A business can show a solid profit on paper and still not be able to pay its staff on Friday. This is not a hypothetical scenario, but it happens to New Zealand SMEs every week. And the problem, almost every time, is that it always comes down to one thing: confusing cash flow with profit, or even worse, thinking that they are the same thing.

You know the basics of running a business if you have been doing it for a few years. But theory and practice are two different things.

This blog gets into the nuances of cash flow vs profit, the stuff that actually trips up experienced operators.

Why Cash Flow vs Profit Deservecash flow vs profits More Attention Than It Gets

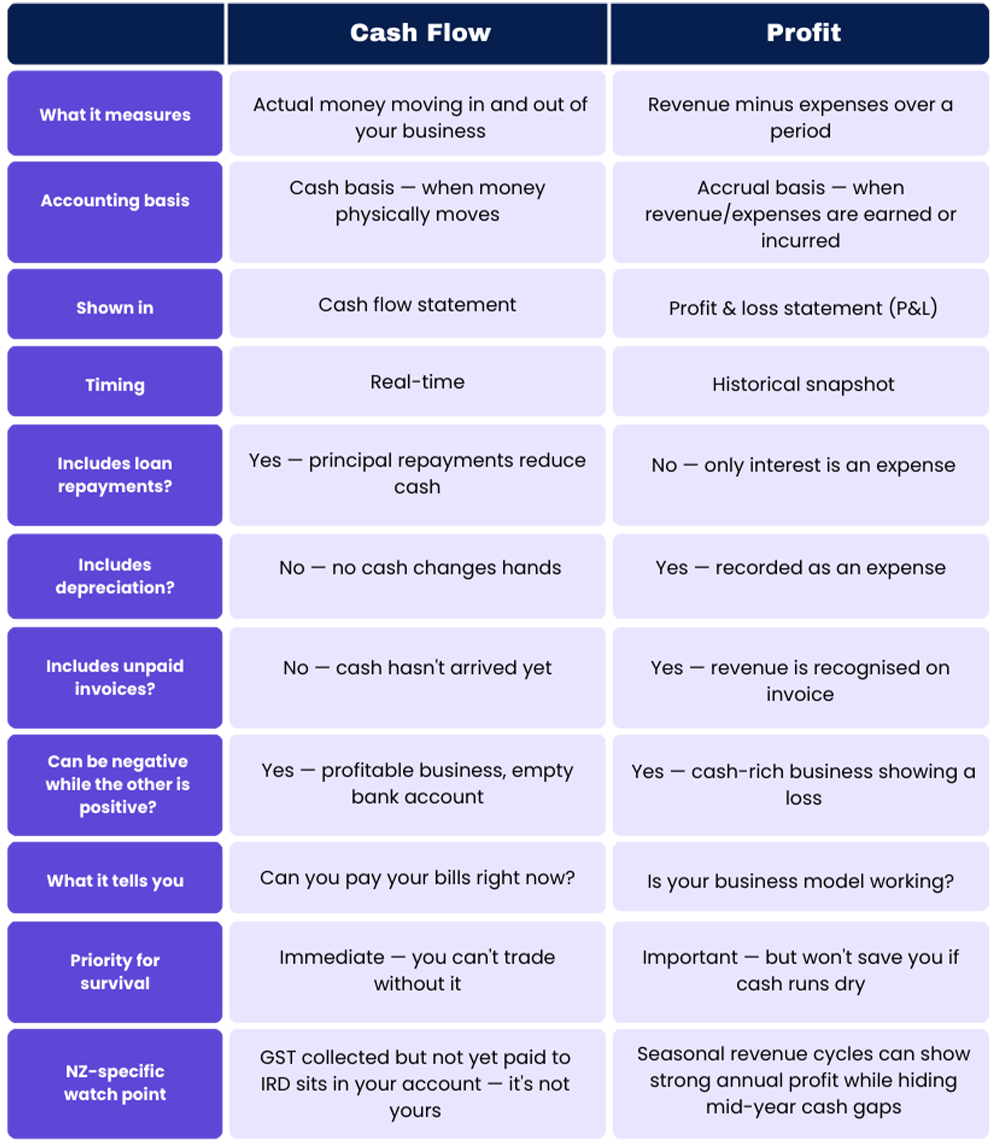

At Bizdom, this is one of the first things we unpack with new clients. Profit is an accounting concept. Cash flow is a survival concept.

Profit lets you know if your business model is a success. Cash flow lets you know if your business will still be open next month. Both are very important, but they measure two completely different things, and they don't always correlate.

Your profit and loss statement shows your revenue when it's earned and your expenses when they're incurred. But your bank account only cares about when money actually moves. That gap between the two is where businesses get into serious trouble.

Here's a scenario that plays out constantly in the NZ market: a trade business wins a big commercial contract. The job takes 90 days. They invoice on completion. But they've been paying for labour, materials, and fuel the whole time. On their P&L, the job looks profitable. But for three months, they've been running that work off their own cash reserves, and if those reserves run dry, the business hits a wall, profitable or not.

That's the cash flow vs. profit problem in its rawest form.

The Numbers Game: How Profit Can Mislead You

Profit is calculated using accrual accounting. Revenue gets recognised when the sale happens, not when the cash arrives. Expenses get recorded when they're committed, not necessarily when they're paid.

So what looks healthy on a P&L can tell a very different story in your bank account.

Some of the most common distortions:

Debtors sitting too long

You've made the sale, recognised the revenue, and your profit looks fine. But your customer hasn't paid yet. In New Zealand, 30-day payment terms are standard, but late payment is extremely common, especially from larger businesses or government contracts. Every dollar sitting in debtors is a dollar not in your account.

Inventory as a cash drain

If you're holding stock, you've already spent the cash to buy it. But that spend doesn't show up as an expense until the stock is sold. Your profit may look perfectly healthy, while your cash position has already taken a hit.

Loan repayments don't touch your P&L

Principal repayments reduce your cash, but they're not an operating expense. So your profit could be positive while debt servicing quietly drains your account.

Depreciation runs the other way

It's an expense on your P&L that costs you no actual cash in the current period, which means it can make your profit look worse than your cash position really is.

Put all of that together, and it's easy to see why even experienced operators get caught out. The two statements are genuinely telling different stories.

Cash Flow vs Profit: The Practical Distinction NZ Owners Need to Make

The simplest way to think about it: profit tells you about the quality of your trading. Business cash flow tells you about the timing of your money.

You can have great trading but terrible timing. You can also achieve moderate profit while maintaining tight cash management, and the second business will outlast the first when things get tough.

For NZ businesses specifically, timing is everything. The local market has a few characteristics that make business cash flow harder to manage than it looks:

Seasonal demand cycles

If you're in tourism, hospitality, construction, or agriculture, you already know this. Revenue bunches up at certain times of year, but fixed costs keep running regardless. Over a full year, the profit might look fine, but the cash flow dip in the off-season can threaten the whole operation if you haven't planned for it.

Concentration risk

Many NZ SMEs rely on a small number of clients. When a big client pays late or disputes an invoice, it creates a disproportionate hole in your cash flow. It won't touch your profit until you write it off, but it hits your cash immediately.

GST timing

This one catches many NZ operators off guard. Depending on your filing frequency, you might collect GST in one period and pay it in the next. That money isn't yours, but it's sitting in your account and is easy to treat as available cash. When the IRD payment comes due, businesses that haven't set it aside can find themselves in a real bind.

What Strong Cash Flow Management Actually Looks Like

Cash flow management is more than just monitoring your bank account. It is understanding the cash flow patterns when money is coming in and when it is going out, and how much time you have at any given time.

Some additional finance tips that are more than just the basics:

Create a rolling 13-week cash flow forecast.

Thirteen weeks will give you enough visibility to identify issues before they become emergencies, but far enough out that the figures aren’t estimates.

Update it weekly. The discipline of doing it forces you to think ahead rather than constantly react.

Keep your GST and tax money separate

Open a dedicated bank account and move the GST portion of every payment across as it comes in. Do the same for provisional tax. Then treat that account like it doesn't exist. This one habit alone prevents a huge number of cash crunches for small NZ businesses.

Shorten the time between spending and getting paid

The faster you can turn cash spent on inputs into cash collected from customers, the less working capital you need to keep the wheels turning. Invoice faster, tighten payment terms, offer early payment discounts, or look at invoice finance to speed up your receivables.

Know your break-even in cash terms, not just profit terms

Most owners know the revenue level where profit hits zero. But what's the revenue you need to cover all your actual cash outflows, including loan repayments, tax, and capital expenditure? That number is usually higher than your accounting break-even, sometimes significantly.

Use your accountant for more than compliance

Too many NZ SMEs only really engage their accountant at year-end for tax. Your accountant should also be helping you build and read cash flow forecasts, stress-test your position, and think through your funding structure. If that's not happening, ask for it or find someone who will.

When Profit Is Up But Cash Is Tight: What to Do

It's something the Bizdom team sees constantly. Sales are strong, the year looks profitable, and yet the bank account is running uncomfortably low.

Growth is actually one of the most common causes of cash flow stress. When you're growing, you spend on stock, labour, and inputs before the revenue comes in. The faster you grow, the more cash you burn getting there. It's possible to grow yourself into serious trouble by spending faster than your working capital can keep up with.

If that's where you are, here's what to look at:

Invoice finance

This lets you access a portion of your outstanding invoices straight away, rather than waiting for customers to pay. It's widely available in NZ, and for a lot of businesses, the cost is well worth the breathing room it creates.

Stock or trade finance

If inventory is the thing tying up your cash, there are facilities built specifically for that. You get the goods, sell them, and repay the facility.

Work both ends of your payment terms

Push to get paid faster by customers, and try to extend terms with your suppliers. Even shifting from 30 to 45 days on the supplier side frees up real working capital.

Talk to your bank early on

NZ banks are far more willing to help businesses that come to them early, with a clear picture of what's coming. If your 13-week forecast is showing a crunch in six weeks, have that conversation now, not when you're two weeks out and out of options.

The Mindset Shift That Changes Everything

The thing that separates financially resilient NZ business owners from those who are constantly stressed about cash is pretty simple: they manage their cash flow with the same energy they put into their sales.

Most owners are relentless about generating revenue. Far fewer are as deliberate about understanding how that revenue actually converts into cash. But when it comes to survival, cash management matters just as much and in a crunch, more.

Profit validates your business model. Cash flow keeps it alive.

Understanding the difference between cash flow and profit isn't an accounting technicality. It's one of the most practically valuable things any NZ business owner can get their head around. The ones who truly get it are the ones who build businesses that last, not just businesses that look good on a spreadsheet for a while.

Quick Answers: Cash Flow vs Profit FAQs

-

Yes. If a profitable business runs out of cash because customers aren't paying, growth is outpacing working capital, or timing mismatches pile up it can become insolvent even while showing a profit on paper.oes here

-

There's no single benchmark, but a reasonable starting point: enough cash to cover at least 8–12 weeks of fixed operating costs, and a 13-week forecast that rarely dips into the negative.

-

The fastest levers are invoicing immediately, chasing overdue debtors hard, deferring anything non-essential, and talking to your bank or a finance broker about working capital options.

-

Both are essential, but cash flow is more urgent. You can weather a period of low profit if your cash is solid. You cannot survive running out of cash, even if the profit figure looks healthy.