How to Improve Cash Flow Management for Small Businesses in New Zealand: A Complete Guide

Cash doesn't care how good last quarter looked on paper. It cares whether there's enough sitting in the account on the fifteenth to cover wages, GST, and the supplier who's been patient for far too long. That's the entire problem with cash flow management for small business, summed up in one sentence. Profit is an opinion, built from estimates and timing choices. Cash is a fact, and it doesn't negotiate.

If your business looks solid from the outside but you're still doing mental maths every second week to work out what clears and when, this guide is written for you. Not the surface-level advice you've already heard a dozen times, but the actual mechanics: what's leaking, why it's leaking, and what to do about it starting this week.

What Cash Flow Management Actually Means for Your Business

Cash flow management is just that: a method of monitoring, planning, and controlling the money that flows into and out of your business. That is all. No fancy terms required. Money comes in through sales, borrowing, or investing. Money goes out through rent, salaries, stocks, taxation, and suppliers. Managing your cash flow means you know roughly when each of those movements will happen, so you're never caught out.

The word "management" is doing a lot of work here. It's not just watching numbers go up and down. It's making decisions early enough that you have options. Do you chase an overdue invoice today, or wait until it becomes a real problem? Do you delay a big purchase by two weeks so payroll clears first? These are cash flow decisions, and they happen constantly, whether you're paying attention to them or not.

Cash Flow vs Profit: Why This Difference Trips Up Even Experienced Owners

Here's where a lot of smart business owners get caught out. Profit and cash are not the same thing, and the difference between cash flow and profit causes more sleepless nights than almost anything else in small business.

Profit is what's left after you subtract expenses from revenue, on paper, over a set period. Cash flow is what's actually sitting in your account, right now, that you can spend. A business can report a tidy profit for the quarter and still not have enough cash to pay the electricity bill. How? Because that profit might be tied up in unpaid invoices, stock sitting on shelves, or a big prepayment you made for materials three months ago.

Cash flow vs profit and loss statements tell two different stories. Your profit and loss statement shows performance. Your cash flow statement shows survival. Both matter, but if you only look at one, make it the cash flow. You can survive a quiet month with a wobbly P&L. You cannot survive a month with no cash to pay your team.

This is one of the biggest lessons in business cash flow management: profitable businesses close their doors all the time because the timing of money never worked in their favor.

Why Cash Flow Management for Small Business Matters More in NZ

New Zealand's small business landscape has a few quirks that make this even trickier. We're a small, spread-out market with a lot of businesses relying on a handful of clients or a seasonal trade. Add in GST payments, provisional tax, and the general unpredictability of supply chains from overseas, and you've got a recipe for cash flow surprises if you're not planning ahead.

Provisional tax alone catches out a huge number of Kiwi business owners. You're paying tax on income you haven't fully earned yet, based on estimates, and if your business has grown since last year, that bill can be a shock. With the inclusion of ACC levies, bi-monthly GST filings by the majority of firms, and the gradual accumulation of employee leave payments in the backdrop, one can easily comprehend the necessity of cash flow management becoming a routine practice for small businessmen operating in New Zealand.

Seasonal businesses, like those in tourism, hospitality, or agriculture, face an even sharper version of this. A strong summer doesn't mean much if the cash doesn't stretch through a slow winter. Good cash flow management and forecasting are what turn a seasonal business from a stressful guessing game into something predictable and, frankly, a lot less scary to run.

The Real Reasons New Zealand Small Businesses Run Into Cash Flow Trouble

Let's get specific, because vague advice doesn't help anyone. These are the patterns that show up again and again when a business cash flow problem starts to bite.

Slow-paying customers. You've delivered the work, sent the invoice, and now you're waiting. And waiting. Every day that invoice sits unpaid is a day your business is effectively lending money, interest-free, to someone else.

Overestimating future sales. It's easy to commit to new hires, new stock, or a bigger lease based on where you hope revenue is heading. When that growth is slower than expected, the fixed costs are already locked in.

Underpricing. If your margins are too thin, even strong sales volume won't generate enough cash to cover the gaps between spending and getting paid.

No buffer. Plenty of businesses run so lean that one late payment or one unexpected repair bill throws everything off. A buffer isn't a luxury. It's the thing that keeps a small hiccup from becoming a genuine crisis.

Poor visibility. If you don't know what's coming in the next 30, 60, or 90 days, you're reacting instead of planning. This is probably the single biggest reason cash flow problems catch people by surprise.

None of these are signs of a bad business owner. They're just common traps. The fix isn't complicated, but it does require a bit of structure.

How to Manage Cash Flow: Practical Steps That Work

So how to manage cash flow in a way that actually fits into a busy week running a business? Here's what genuinely moves the needle.

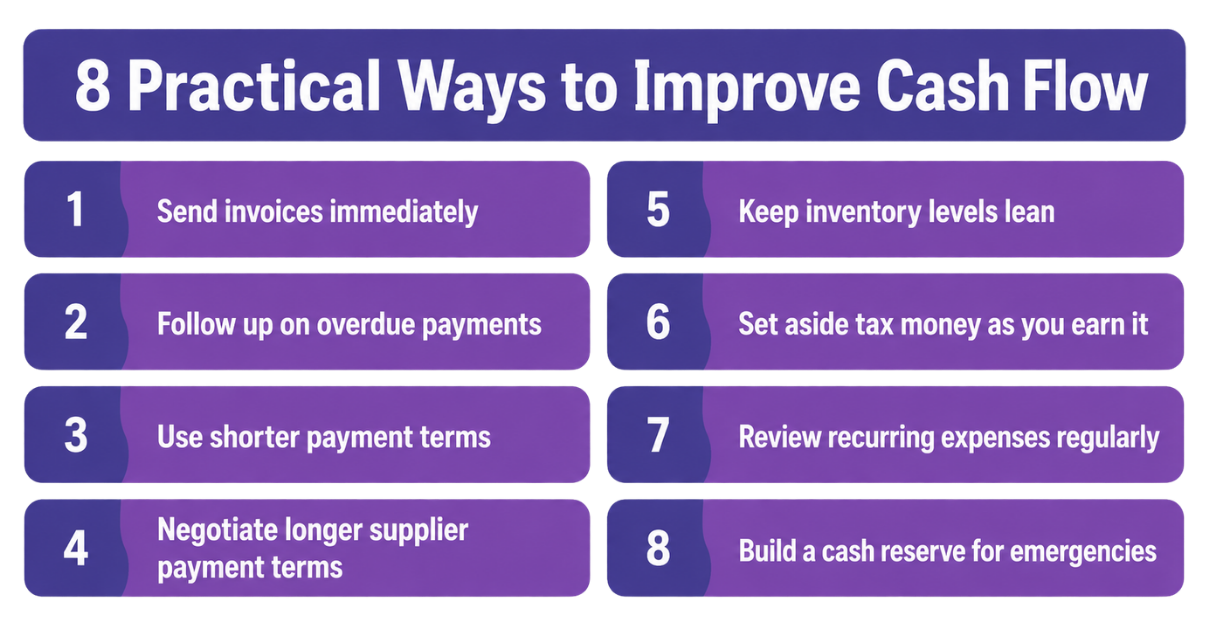

Invoice faster, and follow up sooner. The gap between doing the work and sending the invoice should be as small as possible. Every day you delay invoicing is a day added to your payment wait. Once it's sent, don't be shy about a friendly follow-up at the seven or ten-day mark if payment terms haven't been met.

Tighten your payment terms. Seven or fourteen day terms work far better for cash flow than the standard thirty. If your clients push back, consider offering a small early payment discount instead of long payment windows. It often works out cheaper than the cash flow gap it prevents.

Negotiate supplier terms too. If you're paying suppliers faster than your customers are paying you, that mismatch will drain your cash no matter how good your sales are. Ask for longer terms where you can, especially with suppliers you've worked with for a while.

Keep stock lean. Money sitting in unsold stock is money that isn't doing anything for you. Review what's actually moving and trim what isn't.

Separate tax money as it comes in. Set aside GST and provisional tax in a separate account the moment you're paid, rather than treating it as available cash. This single habit prevents one of the most common cash flow shocks in NZ small business.

Review recurring costs regularly. Subscriptions, software, insurance, all of it adds up quietly. A yearly clean-out of anything you're not using properly frees up more cash than people expect.

Build a cash buffer. Even a small one. Aim for enough to cover a month of fixed costs, then build from there. It changes how you sleep at night, genuinely.

Building a Cash Flow Forecast You'll Actually Use

The importance of a cash flow forecast can't be overstated, yet it's the one tool that gets skipped the most. Forecasting is not meant to be difficult at all. All you have to do is make an educated guess about your income and expenses for the upcoming few months.

Use a spreadsheet or accounting software that creates one for you. List expected income by week, based on invoices due and typical sales patterns. Then list expected outgoings: wages, rent, loan repayments, tax, supplier payments, and anything else recurring. The gap between the two tells you exactly where you stand, and more importantly, where you're heading.

The real value of cash flow management and forecasting isn't in the numbers themselves. It's in the early warning. If your forecast shows a tight patch six weeks out, you have six weeks to fix it: chase invoices harder, delay a purchase, negotiate a supplier deadline. Without a forecast, you find out about that tight patch the week it happens, when your options have shrunk to almost nothing.

Update it weekly if your business moves fast, or fortnightly if things are steadier. A forecast that's three months out of date isn't a forecast anymore. It's a guess dressed up as a plan.

Tools and Systems for Managing Business Cash Flow

You don't need to run everything through complicated spreadsheets. Most modern accounting software, including platforms widely used across New Zealand, includes built-in cash flow tools that pull directly from your invoicing and expense data. This gives you a live picture instead of a once-a-month snapshot.

Look for software that lets you:

See upcoming invoices and their due dates at a glance

Track overdue payments without digging through emails

Automate payment reminders to customers

Connect directly to your business bank account for real-time balances

Generate a rolling cash flow forecast, not just historical reports

The tool matters less than the habit of actually using it. A brilliant system checked once a quarter won't help nearly as much as a basic spreadsheet reviewed every week.

When to Bring in Cash Flow Management Services NZ

There's a point where DIY cash flow tracking stops being enough, especially as a business grows, takes on more staff, or juggles multiple revenue streams. That's usually when it makes sense to bring in outside support.

Cash flow management services NZ providers, including offshore accounting partners, can take a lot of this off your plate. They build forecasts using real financial data, flag issues before they become emergencies, and free up the hours you'd otherwise spend wrestling with spreadsheets late at night. For growing businesses, this isn't an indulgence. It's often the difference between reacting to problems and staying two steps ahead of them.

A good accounting partner will also help you separate the noise from the signal. Not every dip in cash is a crisis, and not every profitable month means you're actually flush. Having someone who understands your numbers deeply, and who isn't emotionally tied to the business the way you are, adds a level of clarity that's hard to get on your own.

Common Cash Flow Mistakes to Avoid

A few missteps show up again and again, so it's worth naming them directly.

Mixing personal and business finances makes it almost impossible to see your real cash position. Keep them separate, always.

Treating your bank balance as your cash flow position is another common trap. Your bank balance is a snapshot. It doesn't tell you what's about to leave your account for wages or what invoices haven't cleared yet. Relying on it alone is like driving while only looking at where you've already been.

Ignoring small overdue invoices because they feel too minor to chase adds up fast. Five small unpaid invoices can equal one large cash flow gap.

Expanding too quickly on the back of one good month, without checking whether the cash flow supports it long-term, is how a lot of otherwise solid businesses get into trouble.

And finally, not asking for help early enough. Cash flow problems are far easier to solve at the first sign of trouble than after three months of digging a deeper hole.

Quick Wins to Control Cash Flow This Month

If you want somewhere to start today, here's a short list that makes an immediate difference:

Send every outstanding invoice reminder you've been putting off

Review your payment terms with your three biggest clients

Set up a separate savings account for GST and tax money

Build a simple four-week cash flow forecast, even a rough one

Cancel or downgrade at least one unused subscription or service

None of these take more than a day to action, and together they shift your cash position meaningfully within weeks.

Final Thoughts

Cash flow management for small business isn't about being obsessive over every dollar. It's about visibility, timing, and a bit of discipline around the habits that keep your business breathing between pay cycles. Profit tells you the story of your business over time. Cash tells you whether you'll still be telling that story next month.

It is important to have accurate forecasts, close the invoice-payment gap, maintain a cushion, and do not hesitate to seek professional help when things become too complex for you during the available time frame. Those organizations that survive in this competitive environment are not those that do not encounter tough times. It is those who foresee them.

FAQs

-

Profit is what's left over on paper once you subtract expenses from revenue over a set period, like a month or a quarter. Cash flow is the real money sitting in your bank account right now, available to spend today. A business can post a healthy profit and still be short on cash if that profit is tied up in unpaid invoices, stock on the shelf, or a prepayment made months ago that hasn't turned into a sale yet. This is why relying on your profit and loss statement alone gives you an incomplete picture, and why smart business owners in New Zealand check both figures separately rather than assuming one reflects the other.

-

Weekly, ideally. Businesses with seasonal or steady income can stretch this to fortnightly, but anything less frequent than that leaves too much room for surprises.

-

Slow-paying customers are the biggest culprit, followed closely by mismatched terms where you're paying suppliers faster than clients are paying you. Overestimating future sales and committing to costs based on hoped-for growth is another common trap, along with running with margins too thin to absorb any bump in the road. In New Zealand, provisional tax and GST catch out a surprising number of otherwise well-run businesses, mainly because that money gets spent before it's set aside. Add no cash buffer into the mix, and even a single late payment or unexpected repair bill can tip a healthy business into a genuinely stressful month.

-

Grab a spreadsheet, or use the forecasting feature built into most modern accounting software. List your expected income week by week, based on invoices already sent and typical sales patterns, then list every outgoing you know is coming: wages, rent, loan repayments, tax, and supplier payments. Subtract one from the other and you'll see exactly where your cash position is heading, not just where it sits today. The real value shows up when you spot a tight patch six weeks out while you still have six weeks to fix it, rather than finding out the week it actually bites.

-

When you're losing hours each week to spreadsheets instead of running your business, or when growth has outpaced what your current systems can track properly, that's your signal. A good accounting partner builds accurate forecasts, catches problems while they're still small, and gives you an outside view that's hard to get when you're emotionally close to every number yourself.